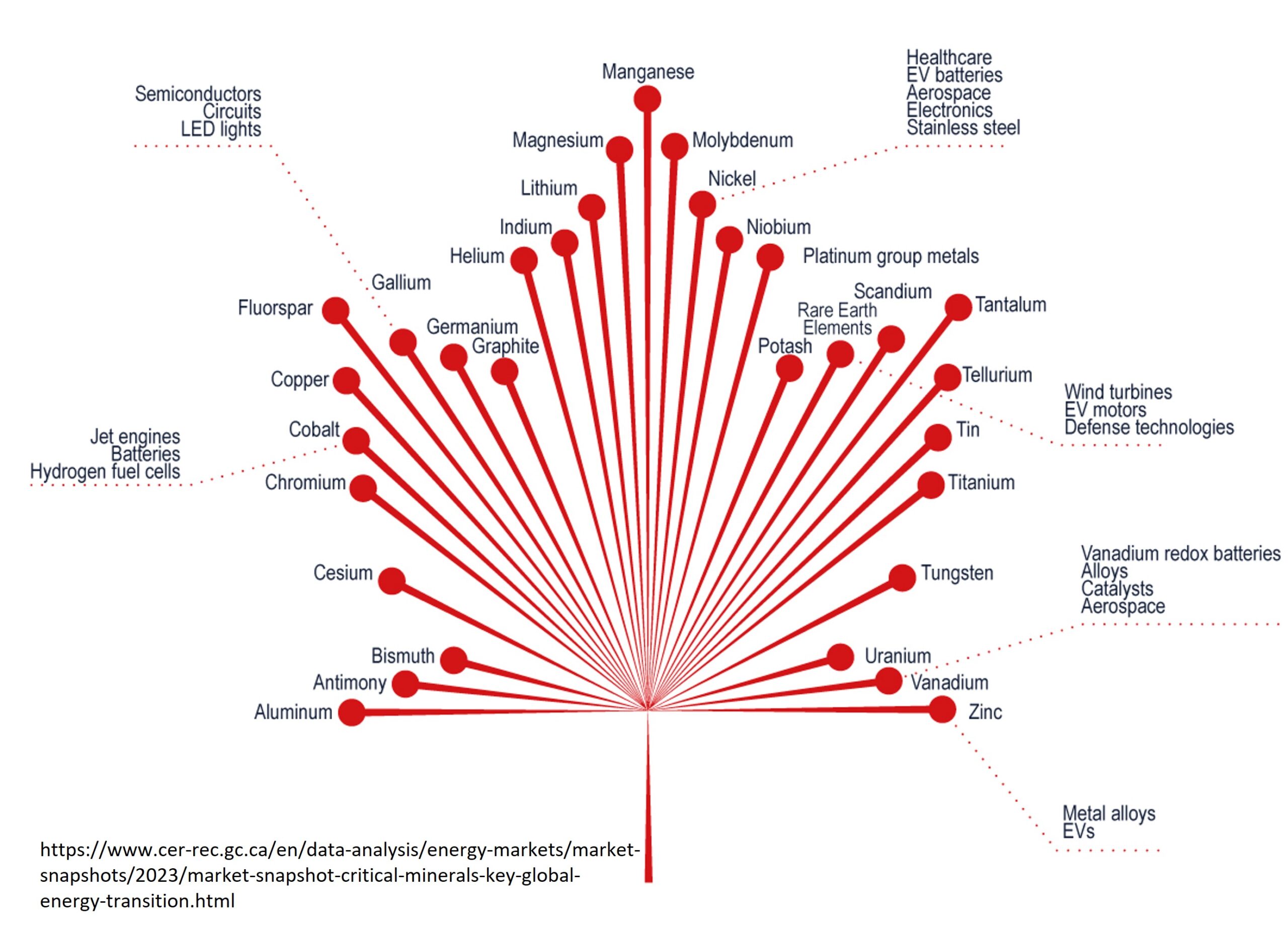

Out of all the ‘critical’ metals, cobalt (Co) is perhaps the most threatened. This rare metal is a vital component of electric vehicles but securing a sustainable supply has proven uniquely difficult. A more diversified supply chain, however, may finally be on the horizon.

Cobalt: A Uniquely Critical Element

For many years Co was an obscure metal mainly used for specialized, highly durable steel alloys, but in recent years it has become an essential component of high-performance batteries, the ones that power electric vehicles in particular. Despite its’ importance the supply of Co is at risk for a number of reasons.

Photo by Alchemist-hp FAL

Unlike most base metals, Co almost never forms its’ own deposits; it’s rare and largely insoluble in the hydrothermal fluids that form most minerals deposits, making it difficult to concentrate to high grades. While most base metals are commonly mined at grades >0.5%, Co rarely exceeds 0.1%. Instead, small amounts of Co are found together with nickel (Ni) and/or copper (Cu) in certain magmatic sulfide, Sediment-hosted Stratiform Cu (SSC), sedimentary-exhalative Cu (SEDEX), Iron-Oxide-Copper-Gold (IOCG), laterite, 5-element-vein, and other deposits. Almost all Co is recovered as a byproduct of Ni and Cu mining.

Without dedicated Co mines, matching supply to demand is difficult, allowing the price of Co to swing dramatically as Co shortages and oversupplies come and go. A metric tonne of Co sold for as much as $82,000 in 2022 but a year later it sits at $35,000, although this is expected to increase in coming years.

To make matters worse, the overwhelming majority (~70%) of global Co production is from the Democratic Republic of Congo (DRC), where large, high grade SSC deposits with weathered, Co-enriched caps are exposed near the surface, allowing easy but largely unregulated mining. This uniquely fertile geology combined with political instability and poverty in the DRC has created a situation where small, primitive mines cause environmental destruction, child labor and safety issues, and criminal activity. The influx of large state-run Chinese companies has alleviated some of these issues, but it has raised national security concerns as China now controls nearly the entire Co supply chain, from mining all the way to battery manufacture. The second-largest Co producer is Indonesia (5%), followed by Russia (5%), Australia and the Philippines (3% each).

The vulnerability of Co supply to disruption has spurred concentrated efforts to find and develop new deposits.

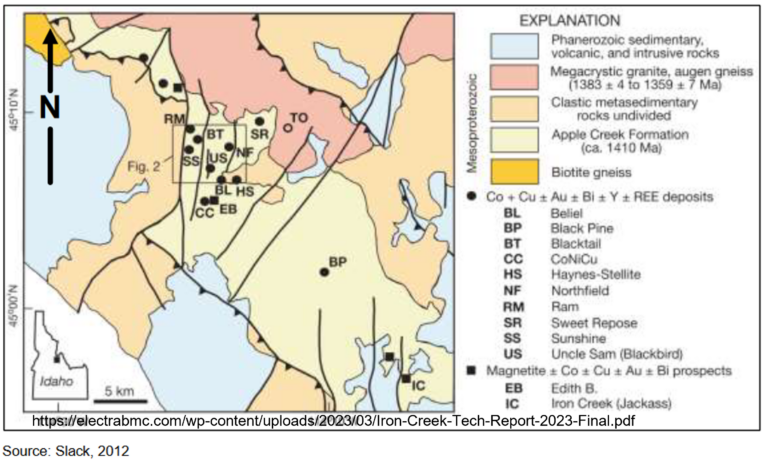

The Idaho Cobalt Belt

The Idaho Cobalt Belt (USA) hosts a number of small, high-grade Co-Cu ± gold (Au) deposits which have attracted considerable interest in recent years. These deposits are generally strata-bound and occur as quartz veins within sedimentary rocks. The origin of Co mineralization in the area is unclear, with SEDEX, volcanogenic massive sulfide (VMS), and, more recently, IOCG models having been proposed over the years. Metamorphism and circulation of hydrothermal fluids may have upgraded Co grades after deposit formation.

Electra Battery Materials (formerly First Cobalt) Iron Creek Project has indicated resources of 4.45 Mt at 0.19% Co and 0.73% Cu and inferred resources of 1.23 Mt at 0.08% Co and 1.34% Cu. Mineralization is hosted in a system of quartz veins. The project is entering the advanced exploration stage, although its’ future is unclear as Electra has pivoted away from mining in favour of becoming a refiner of Co and battery producer.

The partially built Idaho Cobalt Operations project was acquired by Jervois in 2019. It has proven and probable resources of 2.49 Mt at 0.55% Co, 0.8% Cu, and 0.64 G/t gold, plus measured and indicated resources 5.24 Mt at 0.44% Co, 0.69% Cu, and 0.53 g/t Au, making it one of the highest-grade Co deposits known. Life of mine is estimated at 7 years. Production was expected to begin in 2023, however construction was suspended, for the second time, in 2023 due to low Co prices and rising costs.

The Indonesian Ni-Co Boom

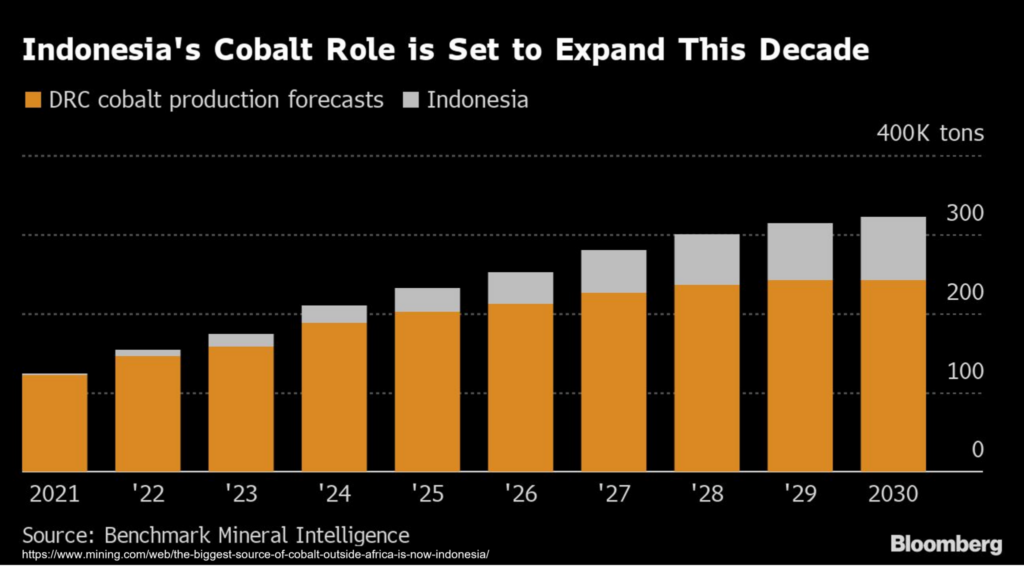

Indonesia has not been a major Cobalt producer in the past, but a massive campaign to develop the country’s mineral resources is already changing the game. Numerous major projects are set to enter production over the next few years, with Indonesia expected to produce 20% of global Co by 2030.

One of the largest and earliest projects is Weda Bay, which is 43% owned by the French mining company Eramet and 57% by China’s Tsingshan Holding Group. Construction began in 2017, with production starting in 2019. Reserves are estimated at 344 Mt at 1.48% Ni and 0.07% Co, with a mine life of 50 years. Laterite ore occurs from surface to approximately 10 depth, making for exceptionally easy open pitting. The project also includes the massive Weda Bay Industrial Park, which contains a High-Pressure Acid Leaching (HPAL) processing plant, a base metal refinery, a ferronickel smelter, and its’ own power plant.

Indonesia has an abundance of Ni and Co laterite ore deposits, which form when Ni and Co bearing mafic and ultramafic rocks are exposed at the surface in a tropical climate. Over time the intense rainfall leaches most of the elements out of the rocks, but Ni and Co are not easily dissolved in water and become concentrated in the remaining material. Indonesia already produces about half the world’s Ni from relatively high-grade saprolite (a form of laterite) deposits, but this new boom is the result of a push to develop lower grade limonite deposits. This ore used to be too low grade to economically process, but the introduction of HPAL technology, combined with billions of dollars of investment by Chinese companies and enabled by strong government support, has changed everything.

Other Sources

The NICO Deposit, Northwest Territories, Canada, is an IOCG deposit with proven and probable reserves of 33 Mt at 0.11% Co, 1.03 g/t Au, 0.14% bismuth (Bi), and 0.04% Cu. It is owned by Fortune Minerals Limited, who plan to mine it via open pit and underground mining. The project would contribute as much as 1% of global Co and 8% of global Bi production per year during its 20-year mine life, but the project has advanced only slowly and intermittently over the last 30 years and it’s unclear when or if production will begin.

The town of Cobalt, Ontario, Canada, has historically been a significant producer of Co from 5-element-veins and is the site of Electra’s Co refinery. There is some exploration activity in the area, but so far no significant deposits have been discovered.

Many Ni-Cu deposits around the world produce some Co, but generally not enough to make a real difference to supply chains.

There is one other untapped source of Co: polymetallic nodules on the seafloor. These potato-sized lumps of almost pure metal occur on the deep, mysterious bottom of the abyssal plains in the Pacific Ocean and are believed to contain enough Co and Ni to replace virtually all inland mining of these elements. The extraction of these mineral riches raises a host of legal, environmental, economic, and scientific issues. The UN agency governing the seafloor in international waters is expected to deliver guidance on how these resources should be treated over the coming months.

Analysis: Will it Make a Difference?

While Indonesia’s mining boom will certainly increase the global supply of Co, it may not do much to make the supply chain more secure and sustainable. The HPAL process is highly energy-intensive and produces particularly toxic wastes; concerns about the environmental impact are already mounting. Most mining companies have avoided the HPAL process due to its’ checkered history of chemical spills and high capital costs. Furthermore, these projects are operated by Chinese companies and will primarily produce Ni with Co as a byproduct: a situation not much different than recent production in the DRC.

Primary Co projects in North America face a very different set of challenges. Their Co grades are much higher than laterites, but their much smaller tonnages and lack of significant co-products makes them vulnerable to volatility in a market which is dominated by vastly larger operations which don’t rely on Co to turn a profit. The rebranding of First Cobalt to the battery manufacturing focused Electra illustrates the challenges of mining primary Co. Even if these Co mines in Idaho and Canada enter production they are unlikely to change the overall Co supply situation.

Bou-Azzer, Morroco, is likely to remain the world’s only primary Co mine for the foreseeable future. The mine, owned by Managem Mines, has been in production since 1928, with Co grades as high as 1%. Very few details of its resources and geology are publicly available.

Investor takeaways

The Co mining game is tricky. The metal is typically extracted as a byproduct of large Ni and Cu mines, leading to difficulties securing a sustainable supply chain and stable price. Although primary Co deposits do exist, they are rare and tend to be small, making them challenging to exploit. Although Indonesia is a rapidly rising Co producer, the rich but problematic deposits of the DRC will remain the world’s main source of Co new discoveries are made, or controversial offshore resources are developed.

List of Companies Mentioned

- Electra Battery Materials: https://electrabmc.com/our-business/iron-creek/ (website)

- Jervois https://jervoisglobal.com/projects/idaho-cobalt-operations/ (website)

- Eramet https://www.eramet.com/en (website)

- Tsingshan Holding Group https://www.tssgroup.com.cn/en/ (website)

- Fortune Minerals Limited https://www.fortuneminerals.com/assets/nico/default.aspx (website)

- Managem Mines https://www.managemgroup.com/en (website)

Further Reading

- Rebecca Tan Dera Menra Sijabat and Joshua Irwandi. The Washington Post. To meet EV demand, industry turns to technology long deemed hazardous https://www.washingtonpost.com/world/interactive/2023/ev-nickel-refinery-dangers/ (website)

Subscribe for Email Updates