There’s a revolution going on in the auto industry right now. Tesla, Inc. has proven demand for electric vehicles (EV’s) and invited the entire industry to join in the fun. From the Bolt to the Volt, from the Focus to the Leaf, pure electric and hybrid cars are pouring off the assembly lines in ever greater numbers. In their own way they are picking a new class of winners in the metals space. This article will briefly discuss some of the rationale behind the excitement and the implications for the demand and use of metals in the future.

Recent forecasts seem to have everyone in the mining sector excited; BHP Billiton estimates there will be 140,000,000 EV’s on the road by 2035, the International Energy Agency estimates 150,000,000. This compares to a little over a 1,200,000 today and means a greater than 11,500% increase in twenty years. This is not including hybrids. Shell is also predicting peak oil demand within the next 5 – 15 years, further supporting estimates for a decline in combustion-powered transportation.

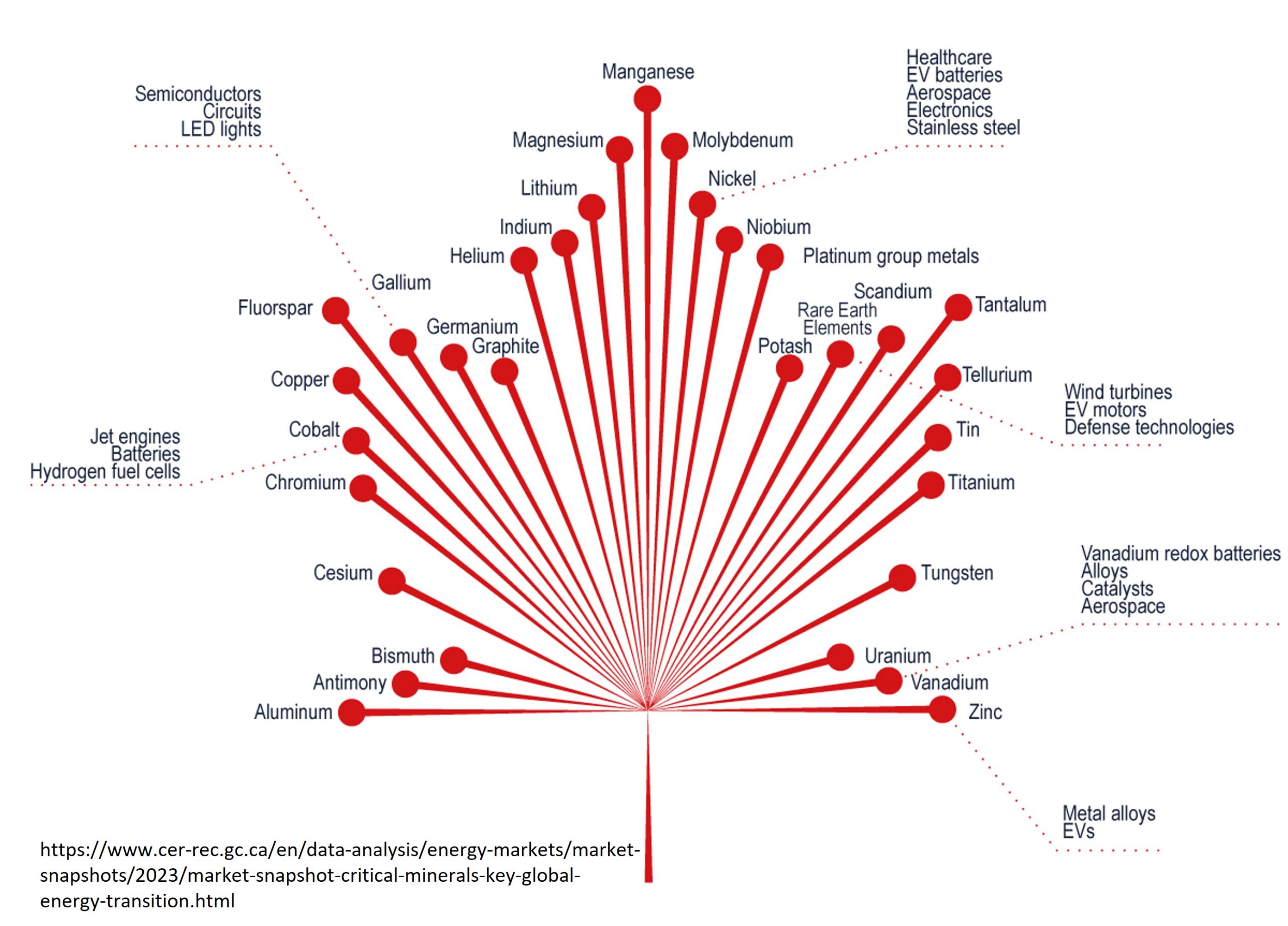

Metal Demand

The metal requirements of each vehicle model and manufacturer can vary depending on the design and manufacturing process. In current Tesla models, lithium, graphite, cobalt, copper, titanium, aluminium and nickel are used. For a Nissan Leaf the battery uses quantities of manganese. Other cars use a different suite of metals including “rare earth elements” in electronics and steel to reinforce the chassis at critical points. What is not needed is a platinum group metal (PGM) catalytic converter, as there is no exhaust to catalyze.

There are some commonly used metals whose demand may increase as EV and hybrid usage and manufacturing increase.

Copper

An average gasoline-powered car uses some 20 kg of copper, mainly as wiring. A hybrid uses 40 kg. A fully electric car uses 80 kg of copper (176 pounds) per car. There is an estimate demand at 11,000,000 tonnes of new copper for EV’s alone, with potential upside in other green technologies. For reference, the entire market for copper for all uses is only 36,000,000 tonnes per annum. This sort of demand could potentially bring lower-grade copper deposits into production.

Lithium

Lithium is a critical component in modern batteries and a source of much excitement lately in the mining sector. A plug in hybrid use about 12 kg of lithium, a standard electric car 22 kg, and a Tesla Model S over 50 kg of lithium per car. A 1% increase in EV penetration into the market would increase lithium demand by 70,000 tonnes per year.

Cobalt

Cobalt is another critical component of current EV Batteries. Use varies by maker, but a Tesla Model S uses about 8 kg of cobalt per battery. Much of the world’s cobalt supply comes from limited reserves in the Central African Copper Belt and these reserves may be depleted in mere decades if EV demand increases as projected. Expect substitution unless new stable supplies are brought into production.

Nickel

Nickel is a critical component in Tesla’s current designs, where the battery cathode is 80% nickel. It is also used in other EV’s to a lesser extent. A shift of 10% of the global fleet to electric cars is estimated to expand the nickel market by 20% from 2,000,000 tonnes per annum to 2,400,000 tonnes per annum.

Graphite

Graphite is a critical component of current battery designs and is a perceived choke point in some supply chain projections. The Tesla Model S uses 54 Kilograms per car currently supplied from China. Graphite is not rare by any stretch. It is a common waste mineral in VMS base-metal deposits and can be found in many other geologic settings. The problem is in purity and quality from these sources, and the currently preferred source for manufacturers is high purity graphite synthesized from petroleum coke.

The opportunity for miners currently lies in high quality, high purity hydrothermal graphite deposits which can meet or exceed synthesized graphite qualities at a lower cost of production and smaller environmental footprint. The graphite market could grow by 93,000 tonnes per annum on EV’s alone.

Rare Earth Elements

Rare Earth Elements (REE) were all the rage a few years ago when China’s near-monopoly and it’s squeeze on the market for rare earths started making the news. Rare earth metals are used in powerful magnets for DC motors by some manufacturers, but Tesla uses AC induction motors that don’t use magnets. Rare earth’s will continue to have a place in specific applications such as electronics and specialized glass, but the existence of alternatives for manufacturers will likely prevent demand and pricing from getting out of hand.

Aluminium

Already a global economic pillar, with many, many uses, aluminum stands to gain some market share from iron as the metal of choice for the body of the car. Much lighter than iron, it allows electric cars to vastly extend their range. Aluminum is not rare and the impact on demand from EV’s is not expected to make much of a dent in the market.

Other Metals

Manganese is used in the batteries of the Nissan leaf and in the Chevy Volt. Manganese is not rare and the metal has under-performed of late.

Titanium is a super hard metal which is used in the undercarriage of Tesla models to protect the battery pack from damage.

The Future

As the old saying goes, necessity is the mother of invention. Innovations in petroleum usage replaced expensive and declining whale oil stocks. Now here we are replacing petroleum-powered transportation with electric vehicles. The EV revolution is in it’s infancy and already in this list above we are seeing substitution and alternative technologies upsetting practical and perceived market demands. Innovation is like that, especially when high costs or limited supply make finding alternatives a necessity. Miners will need to do their own innovating in order to provide future-tech with it’s raw materials at a cost manufacturers can live with.

Further Reading

- Electric vehicles – why all the noise? (BHP Billiton)

- 7 Commodity Winners In Electric Car Revolution (Barrons)

- Induction Versus DC Brushless Motors (Tesla)

- Energy Giant Shell Says Oil Demand Could Peak in Just Five Years (Bloomberg)

- Mining companies have dug themselves out of a hole (Economist)

Subscribe for Email Updates