Aurum. Au. Geld. Gold. The ransom of kings, the symbol of royalty. The economic motor of empires since antiquity and the killer of civilizations. For 5000 years it has held an iron grip on the collective imagination of the western world and shows no sign of letting up. Books and books have been written about the psychological hold this metal has but what of the actual market?

Given it’s psychological importance, the production of gold can be traced deep into history. Gold is found on all continents, in many many different styles of deposit. The main source of global gold production has shifted over the years. In antiquity it was Ancient Egypt and what is now Spain. In the age of exploration it was Latin America and the Spanish Colonies of Peru, Mexico and New Granada (Colombia). In the 19th century it was the placer gold fields in western North America from California to the Klondike provided the bulk of the new production. In the 20th century South Africa dominated the production of gold, reaching a peak of 1000 tonnes a year, and only declined in the last two decades. Now the top spot is held by China with 14% of global production (467 Tonnes) followed by Australia, Russia, USA and Peru. Currently global production averages 2500- 3000 tonnes ( or 85 to 100 million ounces a year). In 2017 gold commanded 48% of the world mineral exploration budget, and many major mining companies are gold exclusive.

Mined production accounts for between 70-80% of annual gold consumption with the remainder of demand fulfilled by scrap gold.

As of 2017 the biggest demand is for jewelry, accounting for a little over half (54%) of the consumption of mined and scrap gold. Currently, India is the biggest market for gold jewelry in the world, with an estimated 22,000 tonnes of gold currently present there and China is a close second. Between the two of them they account for 44% of the world gold jewelry consumption. The balance is demand from the west and with Latin America and Africa taking up the remainder.

Another 36% of gold demand is “investment” which covers gold bullion (bars and coins), financial buying and central bank purchases. Though the gold standard collapsed in the Great Depression and the last vestiges were wiped away in the 1970’s, there is strong allure for keeping gold as an investment vehicle. From central banks to individual investors there is a steady demand for bullion as hedge against inflation or other financial uses. The three main investment buyers are single users, central banks and the gold exchange traded funds( ETF’s). ETF’s and individuals far outweigh the Central banks who only account for 6% of the gold market

The final major use for gold is in electronics and a lesser extent in manufacturing. The conductivity and ductility of gold has made it irreplaceable for everything from high end stereo gear, to smartphones, to jet engines. This accounts for another 9% of current demand with the final 1% going for more exotic uses such as medicine and cuisine.

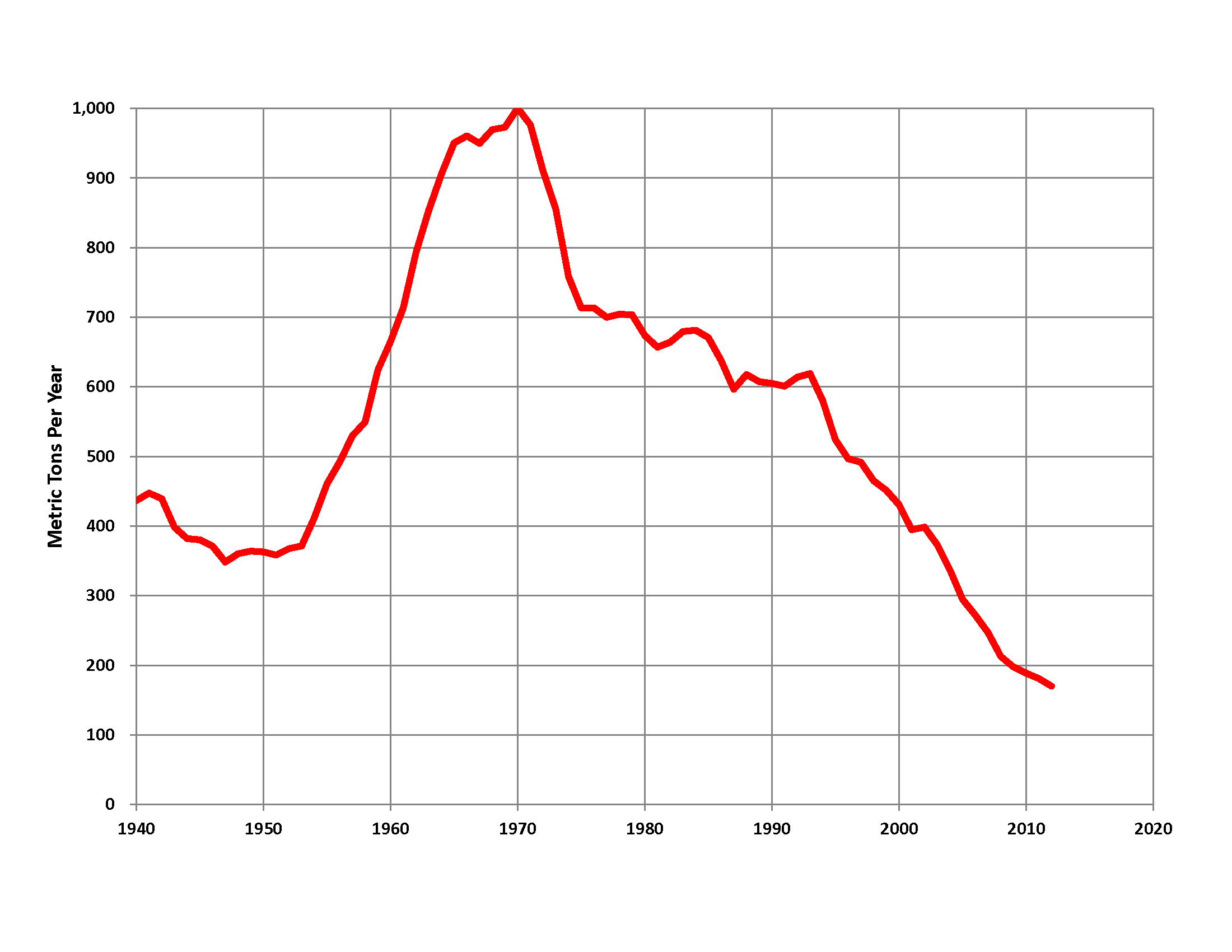

There has been some talk of “peak gold” which is similar to “peak oil” in that as the bigger and richer deposits are mined out, and not replaced then inevitably gold production will dwindle until mine supply falls to zero. This phenomena is apparent in South Africa which reached peak production in 1970 and has slowly declined to less than a 20% of it’s former total. However, humans have been extremely inventive extracting gold from rock, and have brought the average grade of the mined deposit down from the ounce, to the gram, to the 0.2 g/t (200 part per billion) in some cases. Moreover as pure gold deposits wane, gold is increasingly produced as an accessory mineral other deposits. For instance large copper deposits produce millions of ounces of gold a year as an accessory to the copper production. Currently there is no shortage of those, so I expect there to be no shortage of gold for the immediate future.

Further Reading: