The biggest risk to this project by far is China’s state-control of REE prices through export quotas. If the foreign supply of REE’s becomes a threat to China’s virtual monopoly they need only release more into the market and drive down prices.

[box type=”info” align=”aligncenter” ]Disclaimer: This is an editorial review of a public press release and may include opinions or points of view that may not be shared by the owners of geologyforinvestors.com or the companies mentioned in the release. The editorial comments are highlighted so as to be easily separated from the release text. Please view the full release here.[/box]

TORONTO, ONTARIO–(Marketwired – Oct. 23, 2013) – Quest Rare Minerals Ltd. (TSX:QRM)(NYSE MKT:QRM) is pleased to announce that a comprehensive pre-feasibility study (PFS) for its Strange Lake B-Zone rare earth project shows positive results. As envisaged in the PFS, Quest believes that its Strange Lake B-Zone deposit, located in northern Québec, will be one of the world’s largest and highest-grade heavy rare earth (HREE) mining projects and that the planned processing facility in southern Québec will be the largest facility of its kind in North America. Quest’s goal is to provide the growing global market for critical manufacturing inputs with a secure and dependable supply of rare earth elements (REE), given the vagaries of pricing and availability from China, currently the world’s largest source of REE.

[box type=”note” align=”aligncenter” ]A few years ago rare earth elements (REE’s) were all the rage and a lot of the junior miners were looking for REE plays. China is the world’s largest producer of REE’s and was restricting exports in order to pressure manufacturers into setting up shop within Chinese borders. They took state control of the largest REE mines and began shutting down the smaller “illegal” REE mines. Although the buzz over REE’s has subsided somewhat, the issues over China’s virtual monopoly in REE’s is still an issue. More recently, the country has cracked down on illegal exports of REE’s and blacklisted non-complying and suspicious producers. This past month, the US government’s Congressional Research Services published a report discussing the supply and security issues surrounding rare earth metals.

The Strange Lake REE deposit is in northern Quebec near the Newfoundland-Labrador border.

This is a long news release so were going to trim it down a little by placing some of the boring content in toggle boxes.[/box]

Contributors to the PFS were Micon International Limited (Micon International), Process Research Ortech Inc., AECOM, Hatch Associates Ltd., Hazen Research Inc., SLR Consulting Ltd. and RPC. The PFS results show positive cash flows and a robust internal rate of return. With projected average annual rare earth oxide (REO) concentrate production of 13,650 metric tonnes (t), Quest believes that it has the potential to become a significant long-term global supplier of HREE. Based on the PFS, 47% of Strange Lake’s annual rare earth oxide production and 56% of its total revenues will be derived from HREE plus yttrium (HREE+Y) concentrate, which would make Quest one of the world’s leading suppliers of HREE+Y.

The PFS provides for the construction of a hydrometallurgical plant in southern Québec to process whole ore shipped from Strange Lake and to produce four separated products – a mixed HREE+Y oxide concentrate, high-purity zirconium basic sulfate (ZBS, for further downstream processing), high-purity niobium oxide, and a mixed light rare earth double-sulfate concentrate. A mini-pilot metallurgical plant processing 100 kg per day of ore was commissioned in early 2012 to test certain separation processes. Quest is currently preparing for the construction of a full pilot mill, scheduled to commence operation in early 2014.

[box type=”note” align=”aligncenter” ]Niobium and Zirconium are not Rare Earth Elements, but are present in significant quantities in the deposit. They make up more than 30% of the projected mine revenue in this study.[/box]

“We are very pleased with the results of this pre-feasibility study; our consultants have been conservative with the assumptions used and we are satisfied that the returns are very healthy for such a capital-intensive industrial plan,” said Peter Cashin, President and CEO of Quest. “The Strange Lake project has the potential to provide an important base for establishing a major new North American industrial sector, able to address the chronic HREE+Y supply deficit over a long period of time. Over the past three years of intensive work, we have moved the Strange Lake project from a small discovery evaluated on the basis of a limited data set to a substantial mineral development that has grown significantly in terms of footprint and importance to Quest, its shareholders and the industries that are critically in need of the products that Strange Lake will ultimately supply.”

The Strange Lake project dovetails with both Canadian federal and Québec provincial industrial strategies. Quest believes that strategic North American industries from defense to automotive (electric cars) to wind turbines will welcome a stable source of rare earth product. Quest offers a major high-technology industrial opportunity for Québec and Canada with potential for employing many highly-skilled technical and engineering employees. In Quest’s view, the compelling net present value of the Strange Lake project and expected significant amount of product output from Quest’s plant support the required capital investment. Quest believes that the full suite of products, considerable output level and lengthy project mine life will provide key customers with a significant advantage – the stability of North American supply. The successful completion of the PFS marks a major milestone for Quest. Basic engineering for the Strange Lake project is under way. This will allow Quest to accelerate its current discussions with potential off-take and strategic partners for financial and technical commitments to the Strange Lake project.

Quest is committed to ensuring that the Strange Lake mining project sets a high standard for sensitivity to local environmental and aboriginal concerns. Public approval for this project, or its social license to operate, is as important to Quest as are regulatory requirements. The Strange Lake project is designed with a high respect for regional needs and expectations.

PFS Highlights (Table 1):

- The PFS shows a robust internal rate of return (IRR) of 25.6% pre-tax and 21.2% post-tax. The net present value (NPV) of the project pre-tax unlevered with a 10% discount rate is $2.9 billion and $1.8 billion post-tax.

- Total project construction capital costs are $2.57 billion, based on a minimum mine life of 30 years.

- Cash operating costs average $432 million per year, $300 per/t milled.

- [highlight]The project will generate on average $1.047 billion of revenue per year, comprised of 55.8% from the sale of HREE+Y concentrate, 17.3% from the sale of zirconium product, 12.9% from the sale of niobium product, and 13.9% from the sale of a light rare earth (LREE) concentrate.[/highlight]

[box type=”note” align=”aligncenter” ]Our highlighting. Note the significant contributions of Niobium and Zirconium. Iamgold’s Niobec Niobium Mine is also located in Quebec and Canada is already a significant source of worldwide Niobium production.[/box]

- Average annual product output is a mixed HREE+Y oxide concentrate containing 2,100 t of HREE oxide and 4,250 t of yttrium oxide, 24,650 t of ZrO2 contained (as high-purity ZBS), 3,200 t of high-purity niobium oxide, and a mixed LREE double-sulfate concentrate containing 7,300 t of LREE oxide equivalent.

- The undiscounted REO basket price is $73.76 per kg. These price assumptions are based on consensus averages by industry peers from 2013 data, current published market prices from industry experts and key REE market analysts; the concentrate sale price used in the PFS includes a 30% concentrate discount to separated oxide pricing.

[box type=”note” align=”aligncenter” ]Quest is using 2013 averages for REE pricing. It would be nice to see some projections that use high and lows over a longer period. REO means Rare Earth Oxide: The concentrates will be in the form of metal oxides.[/box]

PFS – Key Metrics

The PFS results are based on whole-ore, to be mined at Strange Lake, trucked to the Labrador port facility, and then shipped via the St. Lawrence River to a port site which will be located in the Québec City to Montreal transportation corridor.

Table 1: Key Metrics

| Metric | Amount | Units | ||

| Initial Capital Expenditure | $ | 2,565 | $million | |

| Operating Cash Cost | $ | 432 | $million/year | |

| Revenue | $ | 1,047 | $million/year | |

| Economics (Pre-Tax, unlevered) | ||||

| IRR | 25.6 | % | ||

| NPV@8% | $ | 4,014 | $million | |

| NPV@10% | $ | 2,949 | $million | |

| NPV@12% | $ | 2,163 | $million | |

| Economics (Post-Tax unlevered) | ||||

| IRR | 21.2 | % | ||

| NPV@8% | $ | 2,544 | $million | |

| NPV@10% | $ | 1,800 | $million | |

| NPV@12% | $ | 1,252 | $million | |

| Payback Period | 3.5 | years | ||

| Mineral Resource | ||||

| Indicated | 278 | million t | ||

| Inferred | 214 | million t | ||

| Mining | ||||

| Ore Mined and Shipped | 44.66 | million t | ||

| Production Rate | 1,440,000 | t/yr | ||

| Life of Mine (LOM) | 30 | years | ||

| Strip Ratio | 0.34 | waste to ore | ||

| Revenue Break-down | ||||

| HREE+Y(1) Concentrate | $ | 91.89 | $/kg | |

| LREE(2) Concentrate | $ | 19.99 | $/kg | |

| Zirconium Basic Sulfate | $ | 7.35 | $/kg | |

| Niobium Oxide | $ | 42.00 | $/kg | |

| Recovery Rate | ||||

| HREE+Y Average | 83.1 | % | ||

| LREE Average | 80.2 | % | ||

| Zirconium Basic Sulfate | 74.2 | % | ||

| Niobium Oxide | 86.8 | % | ||

| (1) | Heavy Rare Earth Elements (HREE) include Eu, Gd, Er, Tb, Dy, Ho, Yb, Tm and Lu. |

| (2) | Light Rare Earth Elements include La, Ce, Nd, Sm and Pr. |

| (3) | All dollar amounts in the table above are in Canadian dollars. |

Marketing Initiatives and Industry Partnerships

Quest has been working diligently to reduce project risk through various marketing and partnership initiatives. On July 9, 2013, Quest announced that it had entered into a non-binding letter of intent with TAM Ceramics Group of NY, LLC (TAM), a leading U.S.-based marketer and manufacturer of zirconia chemical products. The letter of intent specifies that TAM will agree to purchase up to 24,000 t of zirconia annually. Several samples produced in Quest’s mini-pilot plant were tested successfully as precursors for a variety of value-added products by TAM.

[box type=”note” align=”aligncenter” ]There aren’t likely a lot of customers for Zirconium and a non-binding agreement with one potential customer is hardly something to bank on, but I guess it’s a start.[/box]

Quest has engaged the Helmholtz Institute for Resource Technology (Helmholtz) of Freiberg, Germany and SGS Lakefield Research Ltd. (SGS) of Lakefield, Ontario for peer review of Quest’s metallurgical processes. The Helmholtz Institute has performed its peer review of the front-end metallurgical process and has issued a positive review report. The Helmholtz Institute is currently developing a comprehensive proposal for improvements of the front-end process including ore sorting, flotation and magnetic separation, which is expected to significantly improve project economics. SGS has performed its peer review on the flow sheet and has also issued a positive review report. Both Helmholtz and SGS will submit a proposal for evaluation of the beneficiation, acid leach and chemical separation processes at the full pilot plant scale. Quest intends to work with both groups on a fully-integrated pilot plant expected to run continuously by mid-2014. This pilot facility will continue to operate as a demonstration plant following successful ramp-up.

Quest is also in discussions with potential joint venture partners for the development of separation technology for individual HREEs from concentrates. Potential industrial partners include leading experts in the field of rare earth refining and specialty chemical product manufacturing. Quest’s objective is to have a separation plant operational at the same time as the start-up of its materials processing operation.

[toggle title=”Next Steps and Potential Efficiency Improvements” state=”close” ]

Next Steps and Potential Efficiency Improvements

Quest has identified numerous efficiency improvements to the base case assumptions presented by the PFS which are intended to further reduce project capital and operating costs and increase product yields. These improvements will be evaluated during the definitive feasibility study work to be initiated in early 2014.

Dr. Dirk Naumann, Quest’s Vice-President, Development, and a 30-year veteran in the advanced materials processing industry states, “Processing efficiencies are already being identified. We believe that elements such as improvements to the current process flow sheet, restructuring of the business model into multiple, integrated operating entities, on-site ore beneficiation to reduce product shipping volumes and costs, and the development of an aboriginal-owned operating company to assume control of all ground and marine logistics for the project will collectively lead to improved operating efficiency.”

1. Strategic Business Plans

The PFS assumes that Quest will execute and operate all aspects of the Strange Lake project within a single corporation. However, Quest recognizes that there may be certain financial advantages to structuring the project in separate corporate entities. These entities would include a mining company, a transport and logistics company, a materials-processing company and a separation and refining company, either as wholly-owned subsidiaries of Quest or as joint ventures with industrial partners. There are a number of potential advantages to such an arrangement, including the opportunity to partner with specialized processing or transportation and logistics providers. From a financial perspective, the capital required for the overall Strange Lake project will not change. However, as an example, in the case of transport and logistics, Quest may be required to fund only 30% of the capital in a transport and logistics company, a potential estimated saving of $220 million. This type of corporate structure could significantly improve project IRR and provide greater project planning flexibility.

2. Mine Site Beneficiation

The PFS provides that the ore will be crushed at the mine site, transported by truck to the Labrador port site, and then by ship to southern Québec. One option being evaluated by Quest involves grinding and mineral concentration at the mine site, resulting in less material being transported, with downstream cost savings. This option would involve higher power costs, capital and operating costs at the concentration level, and yield losses through the process. However, any revenue loss from the drop in yield would be positively offset by processing and shipping less material from the substantial ore stockpiles which will be generated at the mine site.

3. Process Improvements

Quest has identified a number of process improvements which have not been incorporated into the PFS but will be part of Quest’s upcoming feasibility study (FS). These improvements include production of an HREE+Y chloride concentrate instead of an oxide concentrate. This step is expected to reduce the operating costs for production of HREE+Y, while producing a concentrate which is an improved feedstock when compared to individual separation processes; production of a niobium concentrate instead of a high-purity niobium pentoxide. There is potential to improve the initial niobium concentrate quality so as to render it suitable as feedstock for ferro-niobium production, and remove the requirement to refine the concentrate in a separate solvent extraction circuit. Producing a concentrate would allow Quest to lower both capital and operating costs and improve overall returns for the Strange Lake project.

[/toggle]

Project Development – Timeline

Quest has established a conservative timeline for executing on its development strategy (Table 2). Several of these initiatives are underway with the goal of delivering first product from Strange Lake in 2018.

Table 2: Timeline

| Social License Consultations, Memoranda of Understanding, Impact Benefit Agreements | 2013-2014 |

| Establishment of Supply and Strategic Development Agreements | 2014 |

| Commence Full Pilot Plant | Q1 2014 |

| Commence Feasibility Study | Q2 2014 |

| Environmental and Construction Permits | 2016 |

| Construction of Facilities | 2016 |

| Completion of Construction and Commissioning | 2017 |

| Delivery of First Product | 2018 |

Review of the PFS Project Development Model

The PFS covers all aspects of project development, including the mining operation and hydrometallurgical materials processing facility, as well as all related infrastructure and logistics. Micon International developed the mine plan based on the resource model published in late 2012. AECOM and Hatch Associates Ltd. developed the capital and operating cost estimates from principal capital quotations and estimates from suppliers, manufacturers and contractors. The process flow sheet was developed with the combined efforts of Process Research Ortech Inc., Hazen Research Inc., Hatch Associates Ltd. and Quest. Some aspects were tested at the mini-pilot plant scale.

General Project Description

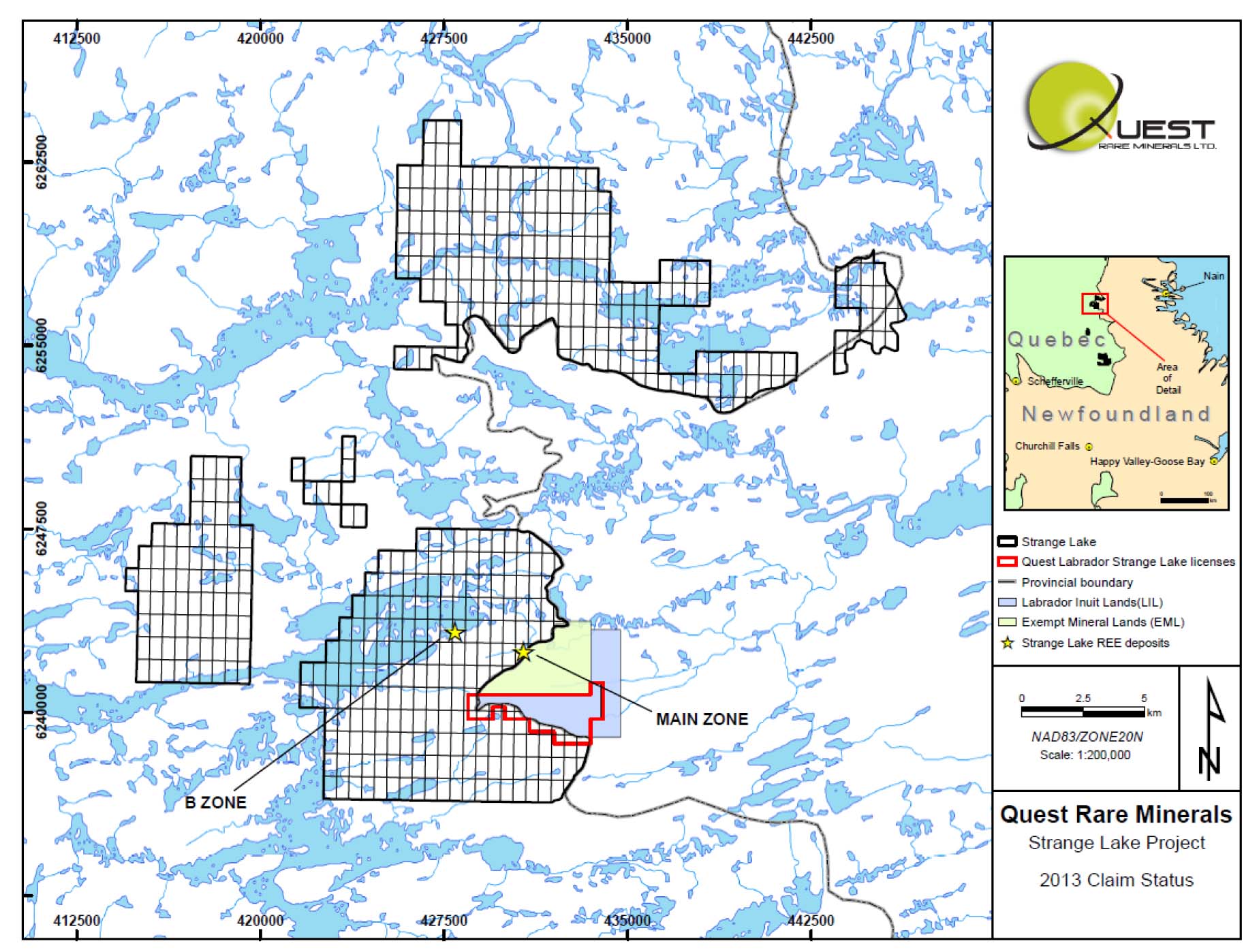

Quest is developing the Strange Lake project in northern Québec. All of the mineral claims comprising the Strange Lake project are 100% owned by Quest. The Strange Lake project is comprised of 552 individual mineral claims covering a total area of approximately 23,680 hectares and is situated approximately 1,100 km northeast of Québec City, the capital of Québec (see Figure 1 in attached Appendix). The project area is accessible by fixed-wing aircraft or helicopter from Schefferville, Québec, or from Nain or Goose Bay, Newfoundland and Labrador. Vale’s nickel-copper mine at Voisey’s Bay is the closest mine, located approximately 125 km east of Strange Lake, on the Labrador coast.

Project Infrastructure

The Strange Lake mine site facilities will comprise an accommodation camp, multi-functional building and maintenance workshop building. Access roads will link the open pit mine with the mine facilities ore stockpiles, waste rock storage, landfill site and airstrip (see Figure 2 in attached Appendix). The port and mine site will be linked by an all-weather gravel access road, constructed over a 168 km distance of flat to hilly terrain. Several port location options are considered in the PFS. The preferred port option includes a floating pier which can receive both smaller vessels and barges that have significantly shallower drafts, allowing the pier to be located close to the shoreline. At the feasibility study (FS) stage, more extensive study will serve to validate and confirm specific port site requirements and configurations.

[box type=”note” align=”aligncenter” ]This project is very remote. Workers will be flown in and out. Quest will have to construct 150+km of road and a port for shipping out the concentrate. This is not without precedent, but it significantly adds to the initial capital costs.[/box]

The PFS provides that the processing infrastructure, which includes the process plant itself and the industrial residue containment facility, will be located in southern Québec. The process plant site will include sulphur storage, an acid plant, solvent extraction (SX) plant, ore stockpiles, utilities and supporting systems. The residue containment facility will include the residue storage structure and the dewatering building and related ponds and piping between the two lots.

[toggle title=”Potential Employment and Skill Requirements” state=”close” ]

Potential Employment and Skill Requirements

The PFS provides that the Strange Lake project will employ a total of 834 employees, comprised of 324 employees at the mine site, 381 at the processing plant in southern Québec and 129 for infrastructure and general administration. Quest will employ engineers, metallurgists and geologists who will require undergraduate and/or post-graduate degrees. Administrative and support staff with undergraduate and/post-graduate degrees will also be employed within finance, human resources, procurement and emergency services. See Table 3 below for the breakdown of employment in each category.

Table 3: Potential Employment Breakdown

| Processing Plant Operations | |||||||

| Jobs | Engineering & Maintenance |

Health & Safety |

Plant | Supply Chain |

Mining | Infrastructure & General Administration |

Total |

| Executive | 0 | 0 | 1 | 0 | 1 | 6 | 8 |

| Professional | 6 | 2 | 8 | 1 | 6 | 1 | 24 |

| Technical | 22 | 2 | 49 | 6 | 23 | 9 | 111 |

| Field Supervisors | 4 | 0 | 9 | 3 | 22 | 10 | 48 |

| Skilled & Semi-Skilled Labour | 75 | 0 | 167 | 4 | 263 | 62 | 571 |

| Administration & Support | 2 | 8 | 0 | 12 | 9 | 41 | 72 |

| Total | 109 | 12 | 234 | 26 | 324 | 129 | 834 |

[/toggle]

Geology

[box type=”note” align=”aligncenter” ]Quest doesn’t discuss the geology in great detail in this report, but essentially the REE’s are hosted in fine grained to pegmatitic (very coarse grained) granites. The silica rich granites will necessitate the requirement of a fairly expensive milling processes to grind the ore. Compare this to the Chinese REE deposits which are hosted in clays, albeit in much lower concentrations.[/box]

The Strange Lake Alkalic Complex (SLAC) lies within the Mesoproterozoic post-tectonic Napeu Kainiut pluton, which includes monzonite, granite, granodiorite and rapakivi-type granitic phases. The SLAC lies along the western margin of the Napeu Kainiut where it is in contact with heterolithic Archean gneiss of the Southeastern Churchill Province. The SLAC, a six to seven kilometer-wide circular intrusion of peralkaline granite, is the host rock of rare earth element minerals of the Strange Lake B-Zone deposit. The B-Zone mineralization occurs within multiple stacked, sub-horizontal sheets and lenses of highly-fractionated and REE-enriched pegmatite and aplite hosted by peralkaline granite. By volume, within the block modeled resource, pegmatites comprise approximately 20% and granite 80%. Quest’s previous experience indicates that REE mineralogy in the pegmatite and mineralized granite is similar, albeit somewhat more complex within pegmatites.

Within the B-Zone, the subsolvus granite is LREE enriched relative to HREE+Y, but in absolute terms, pegmatites exhibit the highest grades and at high cut-off grades, HREE+Y concentrations are equal to LREE concentrations i.e. 50% HREE+Y. Within zoned and differentiated pegmatites, REE concentration increases from the margins of the sheet-like pegmatites inwards and the HREE+Y/LREE ratio also increases inwards. HREE+Y mineralization is concentrated within the volatile-rich cores of these pegmatites and is commonly associated with fluorite and iron-rich (hematite, aegirine, arfvedsonite) zones and generally, where alteration is most intense. Hydrothermal brecciation within these volatile-rich zones may also host high-grade REE mineralization. Although primary REE phases are preserved throughout the B-Zone, replacement textures indicate that secondary minerals comprise the majority of REE mineralization.

Mineral Resource

In 2012, Quest disclosed a revised resource estimate, doubling the tonnage for the Strange Lake B-Zone REE deposit (see Press Release: October 31, 2012, Table 4). The B-Zone deposit currently has an indicated resource of 278,128,000 t at 0.93% TREO, 1.92% zirconium oxide (ZrO2), and 0.18% niobium pentoxide (Nb2O5), and an inferred resource of 214,351,000 t at 0.85% TREO, 1.71% ZrO2 and 0.14% Nb2O5 (see Figure 3 in attached Appendix). The most recent technical report supporting the foregoing resource estimate is available under Quest’s profile on SEDAR and EDGAR.

The Strange Lake B-Zone deposit mineral resource estimate was updated by Micon International, in respect of which a report was filed on SEDAR on December 17, 2012. This resource estimate builds upon the previous work conducted on the Strange Lake property as reported in the May, 2011 Wardrop Technical Report as well as on the subsequent exploration and in-fill drilling conducted by Quest. The mineral resource estimates shown in Table 4 below were calculated using a TREO+Y cut-off grade of 0.50%.

[box type=”note” align=”aligncenter” ]As we’ve discussed before, the difference between a resource and a reserve is essentially a feasibility study. If Quest can establish an economically extractable resource, it will become a reserve. Full feasibility studies are huge undertakings and can make up a significant proportion of a mine’s initial capital cost.[/box]

Table 4: Mineral Resource

| Enriched Zone | Granite Domain | Granite Domain | |

| Mineral Resource Category | Indicated | Indicated | Inferred |

| Tonnage (x 1,000t) | 20,020 | 258,108 | 214,351 |

| TREO+Y (%) | 1.44 | 0.89 | 0.85 |

| HREO+Y (%) | 0.72 | 0.33 | 0.3 |

| HREO/TREO | 0.5 | 0.38 | 0.35 |

| La2O3 (%) | 0.15 | 0.12 | 0.12 |

| CeO2 (%) | 0.36 | 0.27 | 0.27 |

| Pr6O11 (%) | 0.039 | 0.03 | 0.029 |

| Nd2O3 (%) | 0.14 | 0.11 | 0.11 |

| Sm2O3 (%) | 0.036 | 0.024 | 0.023 |

| Eu2O3 (%) | 0.002 | 0.001 | 0.001 |

| Gd2O3 (%) | 0.039 | 0.023 | 0.022 |

| Tb4O7 (%) | 0.009 | 0.005 | 0.004 |

| Dy2O3 (%) | 0.066 | 0.032 | 0.028 |

| Ho2O3 (%) | 0.015 | 0.007 | 0.006 |

| Er2O3 (%) | 0.049 | 0.022 | 0.019 |

| Tm2O3 (%) | 0.008 | 0.003 | 0.003 |

| Yb2O3 (%) | 0.051 | 0.022 | 0.019 |

| Lu2O3 (%) | 0.007 | 0.003 | 0.003 |

| Y2O3 (%) | 0.47 | 0.22 | 0.19 |

| Nb2O5 (%) | 0.34 | 0.16 | 0.14 |

| ZrO2 (%) | 2.59 | 1.87 | 1.71 |

| HfO2 (%) | 0.06 | 0.05 | 0.04 |

Notes:

1. Total Rare Earth Oxides (TREO+Y) include: La2O3, CeO2, Pr6O11, Nd2O3, Sm2O3, Eu2O3, Gd2O3, Tb4O7, Dy2O3, Ho2O3, Er2O3, Tm2O3, Yb2O3, Lu2O3 and Y2O3.

2. Heavy Rare Earth Oxides (HREO+Y) include: Eu2O3, Gd2O3, Tb4O7, Dy2O3, Ho2O3, Er2O3, Tm2O3, Yb2O3, Lu2O3 and Y2O3.

3. Light Rare Earth Oxides (LREO) include: La2O3, CeO2, Pr6O11, Nd2O3 and Sm2O3.

4. The effective date of the resource estimate is August 31, 2012.

5. The resource estimate is based on drill-core assays from Quest’s 2009 to 2011 assay database.

6. Micon International considers a cut-off grade of 0.50% TREO+Y to be reasonable based on a Whittle pit optimization and a minimum marginal economic value of $250 NSR based upon processing and G&A cost estimates for the current block model.

7. Average specific gravity is 2.72 g/cm3 for the Granite Domain and 2.74 g/cm3 for the Enriched Zone.

8. The resource estimate has been classified as an Indicated and Inferred Resource on the basis of data density applying the following criteria:

- Indicated classification was assigned to all resource blocks in the model occurring within the optimized pit shell which fall in areas with a drill spacing of at least 50 m by 50 m and was estimated using at least 16 samples from a minimum of four drill holes.

- All remaining resource blocks in the block model occurring within the optimized pit shell and with an estimated a grade greater than zero were assigned to the Inferred class.

9. The resource estimate takes into account the following:

- A database of 256 drill holes, totaling approximately 37,434 m of diamond drilling, using 22,565 samples.

- Assay values in the database below the detection limit were assigned a value of half the detection limit.

- Samples were composited to a 2 m length.

- A lithology table was provided with codes for each major rock type observed in the deposit, primarily identified as pegmatite and subsolvus granite.

- An NSR value using estimates of the metal prices and recoveries, provided by Quest, was added to the sample assay database.

- A cross-sectional interpretation of the pegmatite lithology was provided by Quest and was used by Micon International to model the wider pegmatite spine and dome structure with some mixing of the interlayered lithologies allowed in order to maintain continuity of the domain along strike and allow for a wireframe construction of the Enriched Zone to be completed.

- The minimum modeled length of the high-grade intervals for the Enriched Zone width was 5 m using a combination of pegmatite lithology indicators and an NSR value with a maximum acceptable internal dilution of 3 m provided the total composite grade remained above a cut-off. An NSR cut-off for the “Enriched Zone” of $725/t was ultimately used as it formed intervals which could be connected between sections and maintained the descriptive statistical properties of the pegmatite.

- Grade capping was applied. In the case of the Enriched Zone, the methodology employed for establishing the outlier limit was to sort the sample populations from smallest to largest and cap to the value where there is a large increment in grade as the population breaks apart. In the granites the outlier limit was set at the 99th percentile value. This set a lower capping value than in the Enriched Zone so that the isolated high-grade pegmatite samples within the domain do not result in local grade overestimation or grade smearing.

[box type=”note” align=”aligncenter” ]Quest is talking about their QA/QC process and specifically mentions their effort to avoid grade smearing. Essentially, any outliers including unusually high assays are removed from the data.[/box]

- Block model utilized regularly-shaped blocks measuring (X) 10 m by (Y) 10 m by (Z) 5 m which are rotated at 030º. The block model was limited below a topographic surface created using 1 m contours. Overburden lithology was not included in the block model and was excluded using a digital surface model.

- Inverse Distance modeling was used as the method for grade interpolation in the B-Zone block model as it allows simple variation in the power to account for the different statistical properties shown by the different elements. In the REE oxides which show a high nugget effect the grade interpolation was performed using Inverse Distance squared (ID2). This spreads the estimation weight across the informing composite samples so that the estimation is smoothed, as dictated by a high nugget. In the oxides with lower nugget effect Inverse Distance cubed (ID3) was used which assigns more of the estimation weight to the closer informing composite samples. Discretization to 2 m cells was applied to the grade interpolations to account for the volume variance effect.

[box type=”note” align=”aligncenter” ]Block models are used to define resources. Essentially the deposit is broken down into discreet blocks which are assigned grades based on the drill result database. These 3D blocks and their accompanying ore grades are used to establish the overall size of the resource.[/box]

- The resource estimate assumes 100% recovery.

10. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Mine Plan

The Strange Lake B-Zone mine is designed to be a standard truck and shovel open pit operation (see Figure 4 in Appendix attached) targeted to exploit the highest REE grades possible for the first ten years of production (the Phase 1 pit), which will then be followed by additional lower-grade mineralization for subsequent production years (the Phase 2 pit).

The mine is designed to ship 1,440,000 t of ore per year to the metallurgical processing facility at an average stripping ratio of 0.34 (waste rock: ore ratio) for a minimum 30 year mine life. The mill feed for the current year is mined in the previous year (Table 5). This is to ensure that the mill has year-round availability to process feed.

Table 5: LOM Mining Average

| Total Tonnage Mined | 9,072 | 000 t/yr |

| Daily Tonnage Mined | 50 | 000 t/d |

| Tonnage Shipped | 1,440 | 000 t/yr |

| Low Grade (LG) and Medium Grade (MG) Tonnage Stockpiled | 5,052 | 000 t/yr |

| Waste | 2,580 | 000 t/yr |

| Operating Period | 180 | d/yr |

Ore is mined and crushed at the Strange Lake mine site, and loaded into containers for shipping by truck to the Labrador port, where the containers are loaded onto ships for transport to feed the plant in southern Québec.

[toggle title=”Hydrometallurgical Plant” state=”close” ]

Hydrometallurgical Plant

The PFS includes the construction of a hydrometallurgical plant (see Figure 5 in attached Appendix) which, in the base case, will process whole ore shipped from Strange Lake and produce four separate products – a mixed HREE+Y oxide concentrate, a mixed LREE double-sulfate concentrate, high-purity zirconium basic sulfate (ZBS), and a high-purity niobium oxide.

The PFS provides that at the southern Québec site, whole ore is wet-milled and de-watered before being mixed with sulfuric acid. The acid ore mixture proceeds to the thermal sulfation rotary kiln. Following sulfation, there is an acid recovery stage where excess acid is recovered for recycle back into the process flow sheet.

The PFS also provides that dry sulfated material proceeds to water leach, where the rare earth, zirconium and niobium values are dissolved. The slurry is pressure filtered, and the pregnant leach solution (PLS) fed to a volume reduction circuit before moving to the solvent extraction (SX) process. At the PLS volume reduction stage, the majority of the light rare earths are crystallized out of solution as light rare earth double sulfates.

Light rare earth-depleted PLS then proceeds to zirconium solvent extraction, where zirconium is recovered as a high-purity basic sulfate (ZBS). Wet high-purity ZBS cake will be transported to TAM in Niagara Falls, N.Y., with which Quest has signed a letter of intent for the sale of up to the total output of 24,000 t/y ZrO2 contained. Uranium is also completely removed from the PLS and separated from the zirconium stream in the zirconium SX process. Uranium is precipitated and removed from the system as sodium diuranate, which Quest intends to provide to a uranium producer for reprocessing off-site.

In the PFS, zirconium process raffinate, now free of uranium and substantially free of zirconium, proceeds to an SX circuit for recovery of sulfuric acid before the solution proceeds to niobium recovery. Niobium is initially precipitated as a concentrate and then further refined to produce a 99% Nb2O5 product. Filtrate of niobium precipitation proceeds to thorium removal by solvent extraction. Thorium is completely extracted, stripped, and precipitated with lime. The precipitated thorium proceeds through further effluent treatment before being combined with leached residue and other treated solids and disposed of in the residue disposal facility (RDF).

Raffinate of thorium extraction proceeds to HREE+Y extraction. HREE+Y are extracted as a group and stripped to produce an HREE+Y rich strip solution. In the base case model, HREE+Y are precipitated as a fluoride concentrate and then calcined to produce a mixed oxide. An alternative preferred route, the production of a mixed HREE+Y chloride concentrate, is being developed and is expected to replace the HREE+Y fluoride route in the FS as one of the process improvement measures mentioned above. Value product-depleted process solutions are combined for treatment with limestone and lime. The combined residue is dewatered and residue solids are dry-stacked in an engineered site located near the processing plant. Water from the residue neutralization circuit will proceed through a desalination plant before being recycled. The overall process water balance is slightly negative (zero discharge).

[/toggle]

Capital Expenditure

The PFS estimates the initial start-up capital expenditure to be $2.57 billion (Table 6). The average sustaining capital requirements for the operation (mine + plant) are estimated to be $28 million per year, beginning in the fourth year of production. The initial capital cost includes a 19% contingency cost of $405 million.

Table 6: Capital Expenditure

| Cost Category | Amount ($ million) |

|

| Strange Lake Mine | $ | 123 |

| Mine Access Road | $ | 258 |

| Labrador Port | $ | 56 |

| Process Plant | $ | 363 |

| Solvent Extraction Plant | $ | 597 |

| Balance of Plant | $ | 132 |

| Residue Containment Site | $ | 65 |

| Indirect Costs | $ | 566 |

| Contingency | $ | 405 |

| Total | $ | 2,565 |

[box type=”note” align=”aligncenter” ]Almost a billion dollars in “Indirect Costs” and “Contingency”. These are the kinds of things that would be dissected in a full feasibility study, but can squeak through in a Pre-feasibility study.[/box]

Operating Cost

The average total annual operating cash cost (Table 7) is estimated at $432 million (assuming operating 350 days per year). At a nominal production rate of HREE+Y+LREE+ZrO2+ Nb2O5 at 119 t per day, a combined annual total of 41,500 t of product will be produced.

Table 7: Operating Cost

| Cost Category | Amount ($ million/year) |

Amount ($/t milled) |

||

| Mining | $ | 52 | $ | 36.28 |

| Processing | $ | 64 | $ | 44.24 |

| Solvent Extraction | $ | 174 | $ | 120.53 |

| Transport & Logistics | $ | 114 | $ | 79.63 |

| G&A | $ | 28 | $ | 19.63 |

| Total | $ | 432 | $ | 300.31 |

Annual Production Levels

The expected average annual production of REE products from the combined HREE+Y and LREE concentrates (quoted as oxide equivalents) and chemical-grade zirconia and niobium products over the 30 year initial mine life are set out in Table 8.

Rare Earth Metals Market and Sale Prices

The rare earth elements, a group of metals also known as the lanthanides, comprise the 15 elements in the periodic table with atomic numbers 57 to 71. Yttrium, atomic number 39, is often included with the lanthanides since it has similar chemical and physical characteristics and often occurs with them in nature. The rare earth element content of ores and products is generally expressed in terms of the oxide equivalent, or REO.

Table 8: Annual Production Levels

| Annual Production (t) | |||

| Contained Metal Oxide | Minimum | Maximum | Life-of-Mine Average (30 years) |

| Lanthanum (La2O3) | 1,200 | 1,600 | 1,350 |

| Cerium (CeO2) | 3,300 | 4,800 | 3,850 |

| Praseodymium (Pr6O11) | 400 | 580 | 460 |

| Neodymium (Nd2O3) | 1,200 | 1,800 | 1,400 |

| Samarium (Sm2O3) | 150 | 260 | 200 |

| Europium (Eu2O3) | 10 | 20 | 13 |

| Gadolinium (Gd2O3) | 260 | 530 | 360 |

| Terbium (Tb4O7) | 50 | 120 | 80 |

| Dysprosium (Dy2O3) | 370 | 990 | 600 |

| Holmium (Ho2O3) | 80 | 220 | 130 |

| Erbium (Er2O3) | 240 | 670 | 410 |

| Thulium (Tm2O3) | 40 | 100 | 60 |

| Ytterbium (Yb2O3) | 240 | 640 | 400 |

| Lutetium (Lu2O3) | 35 | 90 | 60 |

| Yttrium (Y2O3) | 2,500 | 7,200 | 4,250 |

| Niobium Pentoxide (Nb2O5) | 1,900 | 4,700 | 3,200 |

| Zirconium oxide (ZrO2) | 21,100 | 28,300 | 24,650 |

Quest collects and analyses supply, demand and price data for the REEs plus yttrium, niobium and zirconium and has commissioned a number of independent studies to support its marketing initiatives. REEs are critical manufacturing inputs for a variety of products, such as magnets, batteries, wind turbines, fuels cells for electric vehicles, automotive catalyst systems, catalysts in petrochemical distillation cracking towers, fluorescent lighting tubes and most display panels. There is virtually no substitute for the use of REEs in a wide range of technologies. Many national defense systems are also REE dependent, including guided missile systems, smart bombs, advanced sonar, secure communication, advanced armor and stealth technologies. There is currently almost no open market for individual REEs. Prices for the heavy REEs, which are mainly produced in China, are set by the suppliers based on Chinese government industrial policies. China has dominated the global supply of rare earths since the mid-1990s, supplying close to 90% of the global demand.

Global trends which have strongly influenced the growing demand for rare earths are miniaturization, particularly of consumer electronic devices, automotive emissions control and energy efficiency. Complicating the picture is the general shift of manufacturing away from the United States, Europe and Japan to China, South Korea and elsewhere. Demand for rare earths within China has grown significantly over the past ten years. Chinese industry is a major user of neodymium, terbium, dysprosium and yttrium in its domestic manufacturing and the Chinese government continues to seek secure supplies of these materials for its own industries. Chinese price setting and reduction of supply is part of this strategy, leading to a deficit in future availability. Strategic North American and European industries, such as the defense industry, are vulnerable to Chinese dominance in REE supply.

The price assumptions used in the PFS (Table 9) for the separated rare earth oxides are based on consensus averages by industry peers from 2013 data, current market prices and data from industry experts. Quest has contracted a study from Roskill Consulting Group (Jan./Aug. 2013) for supply and demand forecasts to 2017 and beyond (the Roskill Study). Other sources consulted for rare earth pricing data include Metal Pages, Asian Metals, key industrial end users and leading research analysts in the rare earth sector. The price assumption for zirconium oxide is based on a combination of current and long-term prices as listed in the Consensus Forecast, The Industrial Minerals Journal, the Roskill Study and the TZMI Sand Report (Sept. 2013), which is a market study on zirconium completed by TZ Minerals International Pty Ltd. under a contract with Quest. The price assumption for niobium is based on the Roskill Study and current published market prices. The rare earth oxide prices used in the PFS are listed in Table 9 below. A 30% discount has been applied to the rare earth oxide prices in the economic analysis to reflect the sale prices of the concentrate products; no discount has been applied to the sale price of the niobium and zirconium products.

Table 9: Rare Earth, Niobium and Zirconium Oxide Prices

| Lanthanum (La) | $ | 9 |

| Cerium (Ce) | $ | 8 |

| Praseodymium (Pr) | $ | 85 |

| Neodymium (Nd) | $ | 80 |

| Samarium (Sm) | $ | 9 |

| Europium (Eu) | $ | 1,000 |

| Gadolinium (Gd) | $ | 40 |

| Terbium (Tb) | $ | 950 |

| Dysprosium (Dy) | $ | 650 |

| Holmium (Ho) | $ | 55 |

| Erbium (Er) | $ | 70 |

| Thulium (Tm) | $ | 1,000 |

| Ytterbium (Yb) | $ | 50 |

| Lutetium (Lu) | $ | 1,100 |

| Yttrium (Y) | $ | 30 |

| Niobium (Nb) | $ | 40 |

| Zirconium (Zr) | $ | 7 |

1. All amounts in the table above are in U.S. dollars per kilogram of oxide.

[box type=”note” align=”aligncenter” ]Three things may help make this mine economic:

First, the deposit is rich in Heavy rare earth elements (HREE’s) which, as shown in the table above, are FAR more valuable than light REE’s (LREE’s). HREE’s include Eu, Gd, Tb, Dy, Ho, Er, Tm, Yb and Lu.

Second, the deposit is rich in Niobium and Zirconium which while not particularly valuable compared to HREE’s are present in large enough quantities to add significant revenue. In addition, they are perhaps less susceptible to political price manipulation since China is not a dominant producer of these elements.

Lastly, the deposit is shallow enough for open pit mining which is significantly cheaper than underground methods. This is already an expensive project without an underground component. [/box]

[toggle title=”Sensitivity Analysis” state=”close” ]

Sensitivity Analysis

The PFS includes an extensive sensitivity analysis on the key parameters of the Strange Lake project. The parameters to which project economics are most sensitive are outlined in Table 10 below.

Table 10: Sensitivities

| Parameters | Change | IRR Impact (%) |

|

| Product Prices | 10 | % | 3.5 |

| Capital Expenditure | 10 | % | 2.2 |

| Yield/Mineral Recoveries | 3 | % | 1.1 |

| Ramp-Up Time | 3 years vs. 2 years | 2.9 |

The process and solvent extraction plants represent 55% of cash operating costs. Project economics are less sensitive to changes in plant cash operating costs – a 13% change in these costs changes project IRR by 1%.

Transport and logistics represent 27% of the cash operating costs and, as a result, project economics are moderately sensitive to changes in transport and logistics costs – a 30% change in transport and logistics costs leads to a 1% change in project IRR.

Reagents or chemicals used in the processing and solvent extraction plants are a significant component (32%) of total project cash operating costs. However, a 10% change in the quantity used or the price of these reagents changes the project IRR by only 0.4%.

With respect to the operational components of the project, the mine comprises a relatively small percentage (12%) of the overall cash operating costs. As a result, the project economics are almost completely insensitive to changes in mining costs – mining cash costs would have to increase by more than 50% to reduce the project IRR by 1%.

The project is largely insensitive to changes in labour, energy or material consumables costs.

The PFS has also examined certain combined scenarios, such as an adverse scenario where prices are 10% lower than projected, capital expenditures are 10% higher, yields/recoveries are 3% lower and ramp-up is longer and slower than the parameters considered in the base case. In that scenario, the project still yields an IRR of 17%, demonstrating the robustness of project economics.

The sensitivity analysis provides Quest with a mechanism to focus on improvement measures including those referred to above, which will influence either project economics and/or reduce project sensitivity to parameter changes.

[/toggle]

[toggle title=”Environment and Permitting” state=”close” ]

Environmental and Permitting

More than two years of environmental baseline studies are nearing completion for the proposed project infrastructure at Strange Lake and along the roadway to the Labrador coast. Considerable effort has already been invested to collect data on both the biophysical and human environments in the study area, at the mine site, along a road corridor of more than 160 km in length and at several sites considered for a new port site. The base line study for the proposed processing plant, residue storage area and associated infrastructure at the southern Québec site was initiated in 2013 and is expected to be completed in 2014. All environmental work is being led by AECOM with support from local aboriginal partners and regional service providers to the greatest extent possible.

The current schedule is to commence the Environmental Impact Assessment (EIA) for all project components in early 2014, after submitting a project description to the relevant government authorities. Five EIA processes are being considered: two in Québec (north and south), two in Newfoundland and Labrador (provincial and Nunatsiavut), and one with the Canadian federal government. Assuming some degree of harmonization between jurisdictions, the EIA studies and associated public consultations are expected to take approximately two years (to 2016). In particular, the EIA process in southern Québec could involve public hearings led by the Bureau d’audiences publiques sur l’environnement (BAPE). The EIA would be followed by a period of up to six months in which to obtain necessary environmental approvals (Certificates of Authorization, permits and licenses) prior to initiating construction. Quest anticipates certain critical path early works permit approvals could take less than two months.

Appropriate mitigation and monitoring plans are already being considered by the project team, dealing with the unavoidable environmental impact of mining, including possible compensation scenarios for any net wildlife habitat loss and project closure reclamation. Quest is emphasizing early project planning and design to minimize any potentially significant effects relative to environmental features and functions. At this time, no major environmental impacts have been identified. This proactive and strategic approach has also helped to improve the efficiency and sustainability of the Strange Lake project.

[/toggle]

[toggle title=”Social Acceptibility” state=”close” ]

Social Acceptability

From the beginning of its exploration program at Strange Lake, Quest established and implemented a corporate policy on environmental responsibility. This has been a basis for initiatives to maintain or improve the environment in which Quest operates, especially at the mine site, including cleaning up of legacy waste from previous land-users to protecting sensitive wildlife during active operations around the camp. Local aboriginal workers were also trained and/or integrated into Quest’s exploration and environment teams. Quest’s CEO Peter Cashin has stated that, “The public approval of this project, or its social license to operate, is as important to Quest as meeting and exceeding regulatory requirements.” The Strange Lake project has been designed to be especially sensitive to regional needs and expectations.

Quest initiated early meetings with certain northern aboriginal leaders in 2008. A series of strategic meetings was undertaken in 2012 to provide all key groups with similar levels of information and a comparable opportunity to ask questions and comment on the initial project concept. In January 2013, draft Memoranda of Understanding (MOU) were presented to potentially-affected aboriginal groups, to serve as a basis for negotiations to commence in 2014 on Impact Benefit Agreements (IBA) or other similar arrangements. The current schedule anticipates resolution by early 2016, which will facilitate the government’s own requirement to consult with aboriginal groups before issuing environmental approvals. Both aboriginal and government stakeholders have been provided with regular updates on the progress of both environmental studies and community engagement.

The social acceptability of the project in southern Québec is being assessed based on comparisons to previous projects of similar size and scope, both locally and internationally, and based on an initial pre-consultation exercise with a focus group of inhabitants from the affected region.

Quest has also met with senior government representatives of all jurisdictions concerned, to anticipate any social acceptability issues or opportunities. In particular, Quest has sought to align with regional economic development priorities and develop relationships with local suppliers that have demonstrated competitive advantages. A mine in northern Québec and a port on the Labrador coast is an opportunity to work with Inuit, Naskapi and Innu workers who have previous experience with natural resource developments in the region.

The proposed processing plant site planned for southern Québec requires a highly-skilled workforce, with extensive experience in heavy industries. Spin-off opportunities to draw other REE-based industries to the region are also being discussed. In 2014, Quest intends to consult with local stakeholders in southern Québec to anticipate their concerns, and will consider changes to the project if necessary, before the official EIA public hearings. Social acceptability will remain at the core of Quest’s business model and will continue to be monitored as part of Quest’s future sustainability reporting.

[/toggle]

NI 43-101 Technical Report and Qualified Persons

An NI 43-101 Technical Report supporting the PFS is being prepared by Micon International under the guidance of Richard Gowans, P. Eng., President of Micon International, who is the Qualified Person for the NI 43-101 report. Quest will file the NI 43-101 technical report on SEDAR and EDGAR within 45 days of the date of this news release. Mr. Gowans has reviewed the pre-feasibility study information described in this news release. All figures in this news release relating to the PFS are subject to final review and verification and may change.

William J. Lewis, P.Geo., Senior Geologist with Micon International, is the Qualified Person responsible for the preparation of the mineral resource estimate described in this news release. The effective date of the resource estimate is August 31, 2012. The NI 43-101 technical report supporting the foregoing resource estimate is available under Quest’s profile on SEDAR and EDGAR.

[box type=”note” align=”aligncenter” ]The biggest risk to this project by far is China’s state-control of REE prices through their export quotas. If the foreign supply of REE’s becomes a threat to China’s monopoly they need only release more into the market and drive down prices until the competing mines are no longer economic. While Quest can hardly mitigate this type of risk on their own, they may benefit from the increasing desire by countries like the US to source strategically important resources outside of China.[/box]

About Quest

Quest Rare Minerals Ltd. (“Quest”) is a Canadian-based development company focused on the advancement of its flagship Strange Lake property (rare earth-zirconium-niobium) in northeastern Québec. Quest is publicly listed on the TSX and NYSE MKT as “QRM” and is led by a highly-experienced management and technical team with a proven track record. Quest believes that its Strange Lake project has the potential to become an important long-term supplier of rare earth elements (REE). Quest’s ongoing exploration program led to the doubling of resource tonnage of the B-Zone deposit on the Strange Lake property. In 2012, Quest filed an updated National Instrument 43-101 Indicated and Inferred Resource Estimate for the B-Zone deposit. In addition, Quest has announced the discovery of an important new area of REE mineralization on its Misery Lake project, approximately 120 km south of the Strange Lake project in northeastern Québec, and is advancing the Misery Lake project. Quest continues to pursue high-value project opportunities throughout North America.

[toggle title=”We’ve skipped some of the boilerplate. You can read it in here.” state=”close” ]

Forward-Looking Statements

This news release contains statements that may constitute “forward-looking information” or “forward-looking statements” within the meaning of applicable Canadian and U.S. securities legislation. Forward-looking information and statements may include, among others, statements regarding the future plans, costs, objectives or performance of Quest, or the assumptions underlying any of the foregoing. In this news release, words such as “may”, “would”, “could”, “will”, “likely”, “believe”, “expect”, “anticipate”, “intend”, “plan”, “estimate” and similar words and the negative form thereof are used to identify forward-looking statements. Forward-looking statements should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether, or the times at or by which, such future performance will be achieved. No assurance can be given that any events anticipated by the forward-looking information will transpire or occur, or if any of them do so, what benefits Quest will derive. Forward-looking statements and information are based on information available at the time and/or management’s good-faith belief with respect to future events and are subject to known or unknown risks, uncertainties, assumptions and other unpredictable factors, many of which are beyond Quest’s control. These risks, uncertainties and assumptions include, but are not limited to, those described under “Risk Factors” in Quest’s annual information form dated January 25, 2013, and under the heading “Risk Factors” in Quest’s Management’s Discussion and Analysis for the fiscal year ended October 31, 2012, both of which are available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov, and could cause actual events or results to differ materially from those projected in any forward-looking statements. Quest does not intend, nor does Quest undertake any obligation, to update or revise any forward-looking information or statements contained in this news release to reflect subsequent information, events or circumstances or otherwise, except if required by applicable laws.

[/toggle]

[box type=”success” align=”aligncenter” ]Have a company or release you’d like us to look at? Let us know though our contact page, through Google+, Twitter or Facebook.[/box]

Pingback: Zenyatta Completes Drill Program (Graphite is So Hot Right Now!) | Geology for Investors