As supply chains break down and international relations deteriorate, energy security has rapidly emerged as a vital issue. Several countries, notably France and China, have announced large investments in nuclear energy, which are intended at least partially to secure greater energy security. As the ultimate source of nuclear energy uranium (U) resources are poised to play a key role in energy security and independence.

The Current Energy Crisis

Much of the world finds itself in a self-made energy crisis affecting everything from electricity to gasoline. A combination of under-investment in oil and gas, breakdown of global supply chains, and rising demand has led to the worst fossil fuel supply crunch in a generation. To make matters worse, generation by renewables have been hit by extremely unfavorable weather, even normally stable hydroelectric capacity has been slashed by severe droughts.

The Russian invasion of Ukraine, however, has escalated a challenging situation into a dire one. Russia is the world’s largest exporter of natural gas, and the second largest exporter of oil, and calls to sanction these energy exports have sent prices, and uncertainty, soaring. The situation is particularly severe in Europe, which heavily relies on Russia for the natural gas it needs for heating and electricity; this can’t simply be shut off without causing massive harm to the European economy as well as consumers. This dependance represents a national security risk and a major stumbling block in implementing effective sanctions.

There is no shortage of oil and gas in the ground, but fully replacing Russian energy with other sources will require years and billions of dollars of investment in increasingly unpopular and environmentally questionable fossil fuel infrastructure. This situation is already forcing countries such as Belgium and Germany to reconsider energy policies that prioritize reducing or eliminating nuclear power.

Nuclear power has some unique advantages when it comes to energy security. The extremely high energy-density of its’ uranium fuel allows years’ worth to be stockpiled, stabilizing electricity prices and safeguarding generation capacity. Furthermore, the price of U only accounts for a few percent of generation costs, effectively insulating consumers from U supply shocks. This is in sharp contrast to gas power plants, where fuel must be supplied continuously and sudden increases in gas prices are immediately and directly passed on to consumers unless governments intervene. Reactor operation is also independent of weather, climate, and other local variables. The U and nuclear fuel supply chain, however, is not without vulnerabilities.

Uranium Production

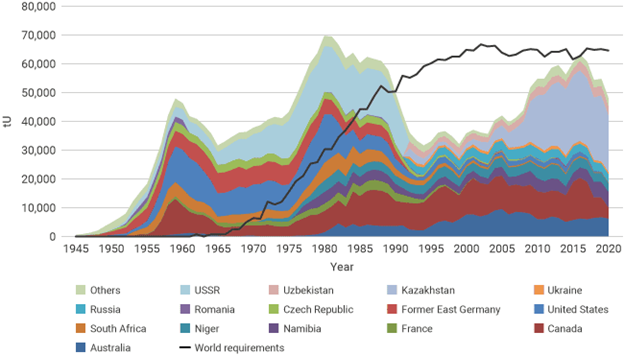

Global U demand has outpaced production for many years, with the shortfall being made up by stockpiled supplies and recovery from tailings and other wastes. The recycling of weapons-grade material from dismantled nuclear warheads alone was enough to meet a large fraction of global demand for more than a decade after the cold war. These supplies are now either exhausted or running low, and the need for increased production has led to a steady rise in the price of U over the last year. Since the war began there has been an additional ~30% spike in the U spot price to more than $60/lb, which has translated into rising stock prices for many uranium producers and exploration companies.

In 2020 three countries produced over two thirds of the world’s uranium: Kazakhstan (41%), Australia (13%), and Canada (8%), with Niger, Uzbekistan, Namibia, and Russia also being significant producers. This picture, however, may be about to change.

Rosatom, Russia’s state-owned nuclear company, has been flagged as a potential target of western sanctions, which would effectively remove Russia’s production from the market. Rosatom is also responsible for about 40% of global nuclear fuel production, including ~16% of fuel imports to the US and ~20% of European imports. While it now seems unlikely Rosatom will be sanctioned, Russia itself has threatened to cut off nuclear fuel exports.

Although Kazakhstan is not directly involved in the war, it is conceivable that geopolitical events could disrupt U supply from the world’s largest producer. Kazakhstan maintains close ties to Russia, with Rosatom holding joint ventures in several Kazak mines, and the country has also experienced substantial political unrest in the last year. Geopolitics aside, current production rates are rapidly depleting high-grade reserves, and Kazakhstan’s very high production is unlikely to be sustainable in the long term.

Supplies from Canada and Australia are much more secure and are poised to ramp up production in the intermediate term. Cameco has announced plans to gradually reopen the McArthur River mine, which will approximately double Canadian U production, meeting a sizable fraction of world demand by itself once it returns to full production in 2024. In Australia, Boss Energy’s much smaller Honeymoon Mine, which has been shuttered since 2014, may also return to production.

Persistently low U prices have discouraged intensive uranium exploration and mine development for several decades, and chronic under-development may lead to a supply gap in the coming years. At full production Cameco’s reserves could be depleted within 15 years, which would eliminate Canadian production from world markets if new mines were not developed in time. Today, only one such mine, NexGen Energy’s Rook Project, is currently in the development stage in Canada. Avoiding a global shortfall will require several new mines of this size to at least begin development over the next decade.

Future U Resources

While poor long-term planning may result in a temporary U shortfall, the very long-term outlook is more positive. Significant unexploited U resources are known, particularly in northern Canada, and large undiscovered deposits are almost certain to exist as well. Assuming a U price of 130 USD/lb, close to the top of its historical price range, global U resources are estimated at approximately 5 Mt, enough for well over 100 years at current consumption rates. Even if there were a dramatic increase in new nuclear development, the long construction times and predictable U requirements of these projects should allow new sources of U to be developed in time.

Over a dozen U deposits styles are recognized, however modern production is dominated by sandstone and unconformity deposits which can be economically mined at very low U prices. Very large amounts of U are known to be contained in resources which have not been mined on a large scale, but theoretically could become major sources in the future. Phosphate rocks, which are mined in enormous volumes for fertilizer, typically contain 50-200 ppm U, which is close to the concentration in some low-grade deposits. Extraction is currently too expensive to economically viable, but this may change if U prices rise, or extraction technology improves. The ash leftover from burning certain coals similarly contains large volumes of very low-grade U which may one day be extracted.

Perhaps the most interesting unconventional U resource is seawater. Seawater contains only 3 parts-per-billion U, but the oceans are so vast that this still represents a staggering 4 billion tonnes of U, making it by far the largest U resource on Earth. This would be enough to meet global energy demand for over 1000 years, perhaps even infinitely once the natural recharge of U weathered from rocks into the oceans is considered. Extraction from seawater would theoretically allow any country with a coastline and the technological capacity to extract and utilize U to become energy independent.

Laboratory experiments have successfully recovered U from seawater with the use of special U-adsorbing fabrics. The cost of this process is estimated at over $200/lb, making it completely uneconomic at current prices, however research into developing a cheaper process is very active, and has begun to yield promising results.

Uranium resources could also theoretically also be extended by approximately 100 times by recycling the U currently discarded as radioactive waste and depleted U. While the technology to do this largely exists, it has so far not been done at a large scale due to a range of economic, political, and weapons proliferation issues.

Investor Takeaways

Economic, geopolitical, and environmental issues have highlighted the need for more secure and sustainable sources of energy and has renewed interest in the unique advantages of nuclear power. Decades of stagnant U prices appear to be coming to an end as U stockpiles and ore reserves of existing mines run low. Existing stockpiles and reopening of mothballed mines will likely prevent the type of acute supply crunch that has rocked oil and gas markets, but in the longer term there is a real need to discover and develop new mines. Fortunately, global U resources are large and diverse enough to meet current and future needs.

The need to discover new sources of U has lifted the stocks of many U miners and explorers; between a supply shortage, rising demand, and rising international tensions threatening existing supply chains there is a sense that the U market has turned a corner and higher prices may be here to stay.

List of Companies Mentioned

- Cameco https://www.cameco.com/ (website)

- NexGen Energy https://www.nexgenenergy.ca/homepage/default.aspx (website)

- Boss Energy https://www.bossenergy.com/ (website)

- Rosatom https://www.rosatom.ru/en/ (website)

Further Reading

- Saefong, M. P. (2022): Uranium Prices Are Through the Roof as the War Shifts Thinking on Nuclear Power. Barrons. Retrieved from: https://www.barrons.com/articles/uranium-prices-spike-as-war-shifts-thinking-on-nuclear-power-51647505802. (news article)

- World Nuclear Association (2021): https://www.world-nuclear.org/information-library/nuclear-fuel-cycle/mining-of-uranium/world-uranium-mining-production.aspx (website)

- Cameco (2022): https://www.cameco.com/ (website)